Commercial Vs. Personal Auto Insurance - What's The Difference?

·

9 minute read

We frequently get calls from small business owners and independent contractors about commercial insurance vs. personal insurance, and what sort of policy they should go with.

While it is true that a commercial auto insurance policy is better equipped to deal with the claims that arise from commercial use of a vehicle, it is also more expensive.

With price being the obvious difference between the two, why would someone want to potentially pay more for a commercial auto policy?

The answer lies in certain coverage and vehicle use exclusions. To find out whether commercial insurance vs. personal insurance is right for you, we explain why people choose commercial auto insurance and address exclusions that could apply to your business.

COMMERCIAL INSURANCE REVIEW

Not Sure If You're Fully Covered? Let's Find Out.

Book a review with our team to uncover hidden risks and see where you can save on your premiums.

Call Now: (918) 664-7100If you do decide to go with a commercial auto policy or want to know more about which policy is right for you, check out our insight “Personal Use Of Company Vehicles: What To Know.”

When do you need a commercial policy?

You Are Making Business Deliveries

If you are making business deliveries in a vehicle and have a personal auto insurance policy, you are probably not covered for liability, physical damage, medical payments (personal injury protection in some states), or uninsured motorists.

There are two exclusions and limitations that could apply to your business:

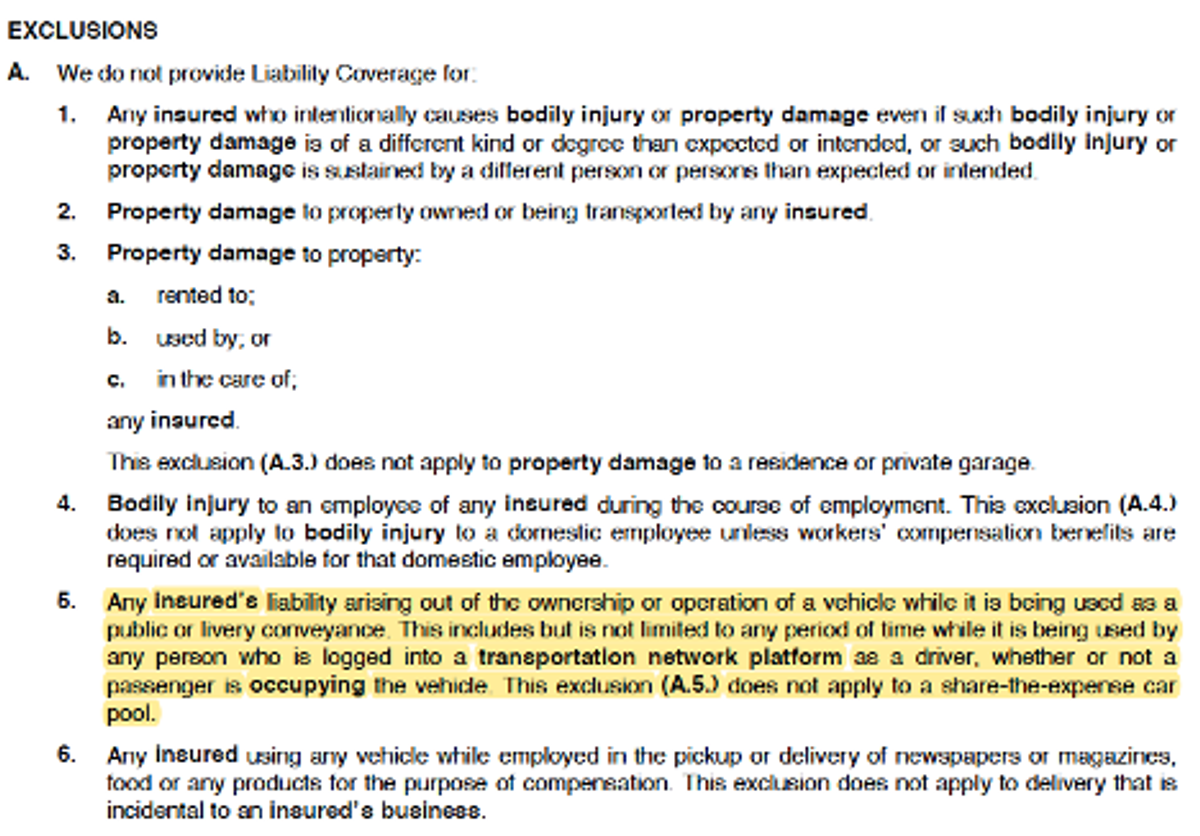

Public Or Livery Conveyance Use Exclusion

But what does public or livery conveyance mean? The International Risk Management Institute defines it as: "The transporting of people and/or goods for hire, such as by a taxi service, motor carrier, or a delivery service.

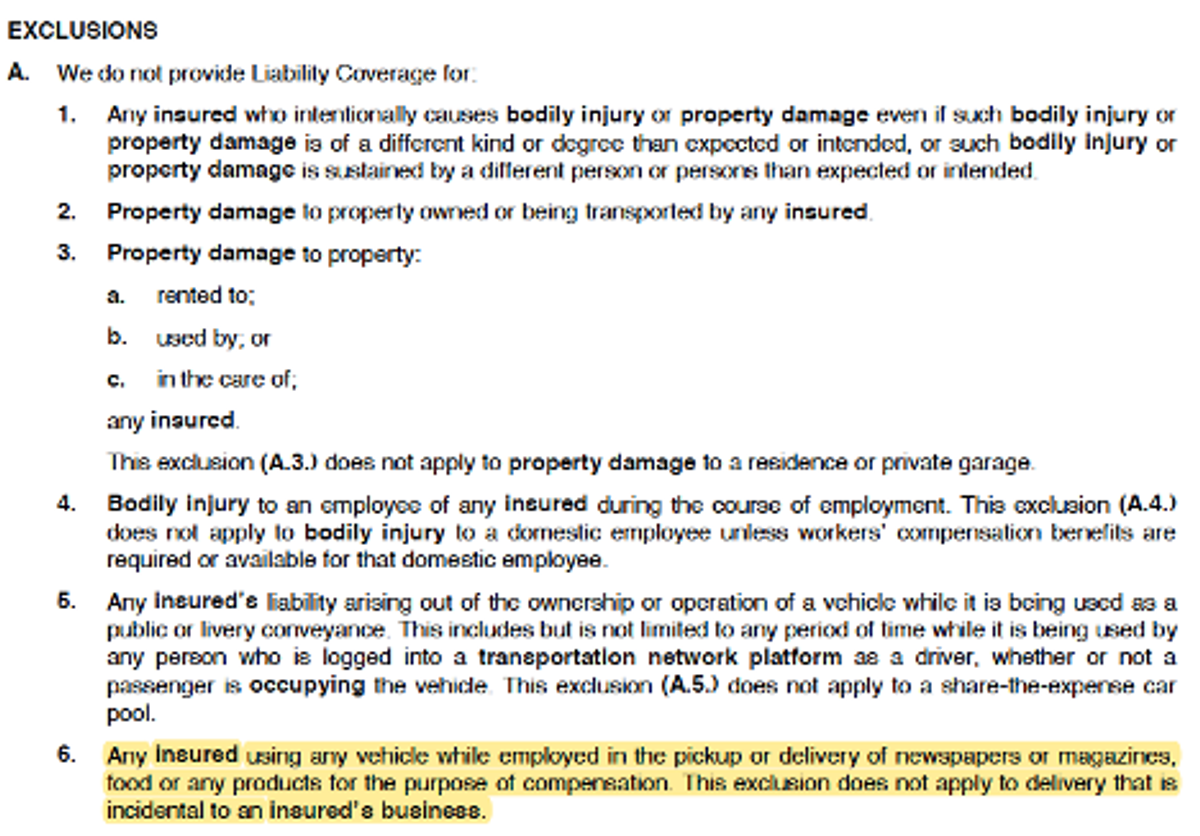

Delivery Of Any Products For Compensation

As you can see, any delivery operations you might have are excluded; even if your business isn’t delivering, per se, it is best not to leave it up to the claims adjuster to decide if delivery is "incidental to your business."

A Business Owns The Vehicle

Having a vehicle titled in a business name is a sure sign that you need a commercial auto insurance policy.

Personal auto policies are not designed to protect and defend corporations from auto lawsuits and settlements. They are designed to defend you, protect your personal assets, and prevent you and your family from experiencing financial harm.

Most personal auto insurance underwriters will not accept submissions from vehicles owned by a business. Additionally, a personal auto policy in your name will not cover assets the business owns.

You Need An Additional Insured Or Waiver Of Subrogation

No matter the industry, customers need certificates of insurance that require their vendors or subcontractors to have certain auto limits and add them as an additional insured.

If you have a personal auto policy, chances are, the underwriter will not only decline the request to add an additional insured, but they will cancel the policy due to commercial auto exposure, too.

If you are taking any work that requires you to submit a certificate of insurance with auto liability coverage, you will likely need a commercial auto insurance policy.

You Have Specialized Equipment Attached To The Vehicle

Many customers have commercial equipment permanently installed on their vehicles, such as booms, lifts, cranes, welders, compressors, etc.

Besides not being able to qualify for a personal auto policy, you may find that a commercial policy would cover your exposures better anyway. From the liability associated with operating your equipment to the physical damage of your expensive attachments, you are better protected under the commercial auto policy.

Loading And Unloading Coverage

The commercial auto insurance policy has coverage that expands the auto insurance to include loading and unloading activities.

This means that if you are unloading your vehicle, your auto policy would cover any damage to property or injuries that occur prior to you placing that object down in its intended spot.

This is a huge reason why many contractors opt for a commercial auto policy. It covers operations outside of operating the vehicle.

What actions can cancel your personal auto policy?

Although not every reason to get a commercial auto policy is the result of an coverage issue, you may not qualify for a personal auto policy without misrepresenting yourself on

the insurance application (which we really don't recommend).

Regular Employee Use

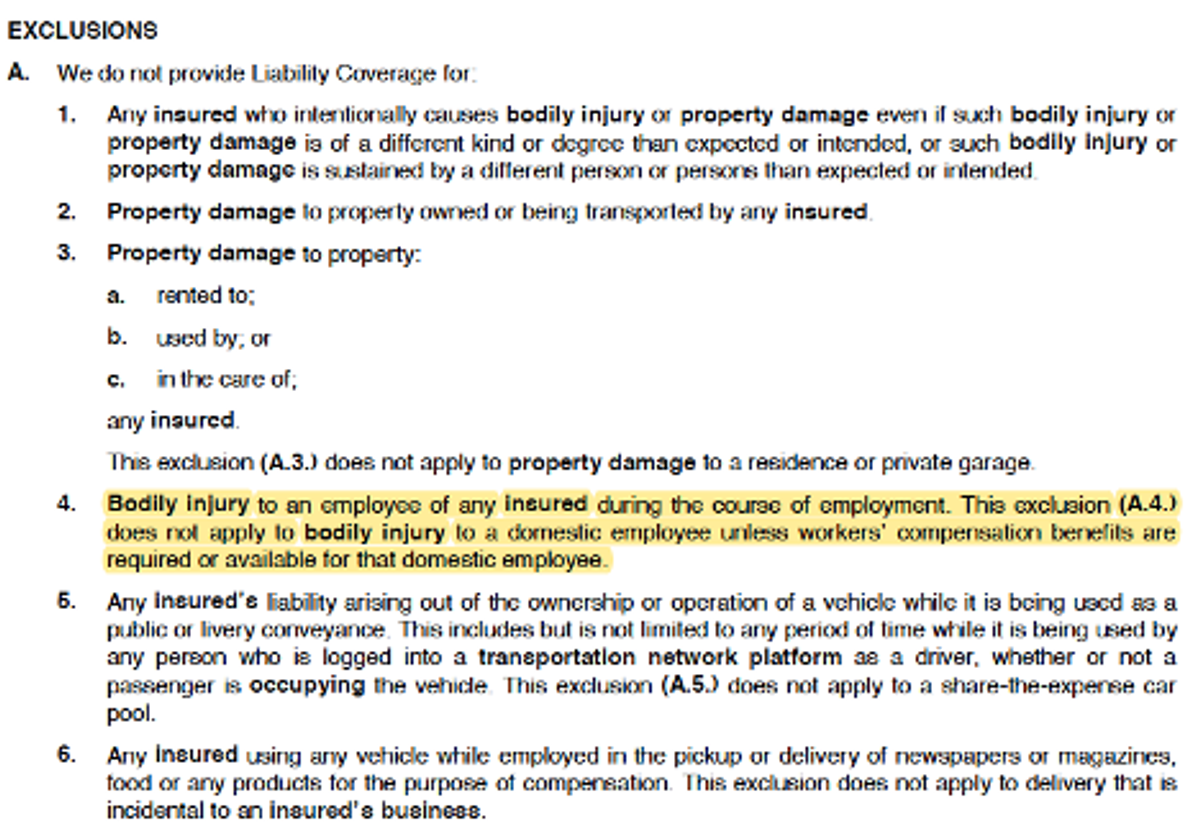

You might have noticed above that there is an exclusion to bodily injury to an employee under the personal auto policy:

But this is an exclusion to bodily injury to the employee, not the liability arising from the employee’s use of the vehicle.

That being said, personal auto insurance companies do not want employees driving your vehicle.

Having a vehicle that others use for your business lowers the ability of the insurance company to adequately price the insurance policy for the others driving the vehicle.

For example, even though you have a pristine driving record and all the safe-driver discounts, you might allow an employee, who has multiple at-fault accidents, to drive your vehicle.

A personal auto policy is not equipped to price for multiple non-family vehicle drivers like a commercial policy would. Additionally, if you have employees driving your vehicle, it is a pretty good indication that you are using it primarily for commercial operations. For this reason, this is a deal-breaker for most personal auto insurers.

Business Decals On Vehicle

Having business decals on your vehicle is another reason why most personal auto insurance carriers will not quote your insurance. And if they find out that you do have decals, they will cancel your policy.

Additionally, if you have business decals on your vehicle and have an accident, it will raise red flags to the claim adjuster. They will know they need to figure out what you were doing and if those activities fall under any of the commercial purposes exclusions.

When do you need a personal auto policy?

Rating a personal vehicle for business use is a popular way to save money on auto insurance. For those that don't have professions that warrant the commercial coverage of a commercial auto policy, you can purchase a personal auto policy and include business use in your activities.

Here are the instances in which you would want to

consider this:

You Only Use The Vehicle For Commuting And Sales Calls

If you are only driving to and from work (even as a business owner), you do not need a commercial automobile policy.

This is the same for doing sales calls, product demos, or consultation visits in a vehicle that you own personally. Just make sure to tell your insurance broker what your profession is and how you will be using the vehicle.

Your Work Doesn't Require Certificates of Insurance

If your work doesn't require that you provide certificates of insurance to work or get on client sites, a personal auto policy with business use might be the right solution for you.

Although you might not have requirements for high limits, we always suggest increasing your liability limits. Oftentimes, if you get into an accident while conducting business, your business or employer could also get involved in the lawsuit. You want your personal auto limits to be high enough to cover both entities.

We recommend at minimum having a 100/300/100 policy. That means you have $100,000 bodily injury per person and $300,000 in total. You also have $100,000 in property damage coverage.

That being said, we still think this is underinsured for most situations and recommend purchasing a $1,000,000 umbrella to cover additional liability exposures.

Summary

There is a fine line when it comes to determining whether you need a commercial or personal auto policy. You need to make sure that the policy covers your business operations and that you abide by the guidelines of each policy.

If you need help determining whether you need a commercial or personal auto insurance policy, let us know. We will look over how you are using the vehicle and help you determine which policy is right for you.

About The Author: Austin Landes, CIC

Austin is an experienced Commercial Risk Advisor specializing in and leading LandesBlosch's design professional, real estate, and construction teams.